Property Management Done Right: A No-Nonsense Guide for Landlords

I’ll never forget my first rental property. It was a duplex I snagged when I was just getting started, and I honestly thought it would be a breeze. You know, collect some rent, maybe fix a leaky faucet here and there, and just watch the money roll in. The reality? So much more complicated.

In this article

I made just about every mistake in the book, learned some tough lessons, and pretty quickly realized that managing a property isn’t some weekend hobby. It’s a full-on business that requires a professional mindset and a solid grasp of some core principles. This isn’t about finding some magic shortcut. This is about laying the right foundation so you can build real, long-term wealth instead of burning out from tenant drama and surprise expenses.

1. The Legal Stuff: Don’t Skip Your Homework

Before you even dream of putting a “For Rent” sign in the yard, you have to get a handle on the laws that will govern your business. Seriously, ignoring this is like building a house on sand. It’s going to crumble, and when it does, it could take your finances down with it. Landlord-tenant law isn’t there to make your life hard; it’s a rulebook that protects everyone involved.

Federal, State, and Local Rules

You’re juggling a three-layer cake of laws, and you need to know what’s in every layer.

First up is the big one: The Fair Housing Act. This federal law is non-negotiable and forbids discrimination based on race, color, religion, national origin, sex, disability, or familial status (which means having kids). This rule touches everything from how you write your rental ads to how you screen applicants.

A simple mistake here can be a disaster. I once saw a new landlord get into hot water over a seemingly innocent ad. He described his one-bedroom unit as “perfect for a single professional.” A family with a small child applied, got denied, and filed a fair housing complaint. They argued the ad showed a bias against families. The lesson? Always describe the property, not the person. Stick to the facts like “one-bedroom unit on the third floor,” and let people decide if it fits their needs.

Then you have state and local laws, which get into the nitty-gritty of day-to-day operations. These rules can vary wildly from one town to the next, covering things like:

- Security Deposits: How much can you collect? In my area, it’s two months’ rent. Do you need a separate bank account for it? Many places require it. How long do you have to return it after a tenant leaves? For me, it’s 30 days. Get this wrong, and you could owe the tenant double or even triple the deposit amount.

- Right of Entry: You can’t just pop in whenever you want. Most areas require “reasonable notice,” which is usually 24 hours in writing, for any non-emergency entry.

- Evictions: This is a formal legal process. You can’t just change the locks or shut off the water. You have to serve the proper notices and follow the court’s procedure to the letter. One tiny error can get your case dismissed, and you’re back to square one while the tenant stays put, rent-free.

Your Lease is Your Shield

Your lease agreement is the most important piece of paper in your entire business. A generic, one-page lease from an office supply store is basically an invitation for problems. A strong, professionally reviewed lease is your best defense.

Don’t be scared by the idea of hiring a lawyer. For my first property, I paid a local attorney about $500 to draft a rock-solid lease agreement tailored to my state’s laws. It was the best $500 I ever spent, especially when you consider that a single messy eviction can easily cost ten times that much. Think of it as a one-time investment in peace of mind.

2. Get Covered: Insurance Isn’t Optional

Your property is a huge investment, and protecting it from risk is just part of the job. A lot of new landlords get confused here, thinking their homeowner’s policy is enough or not understanding what renter’s insurance actually does. Let’s clear that up.

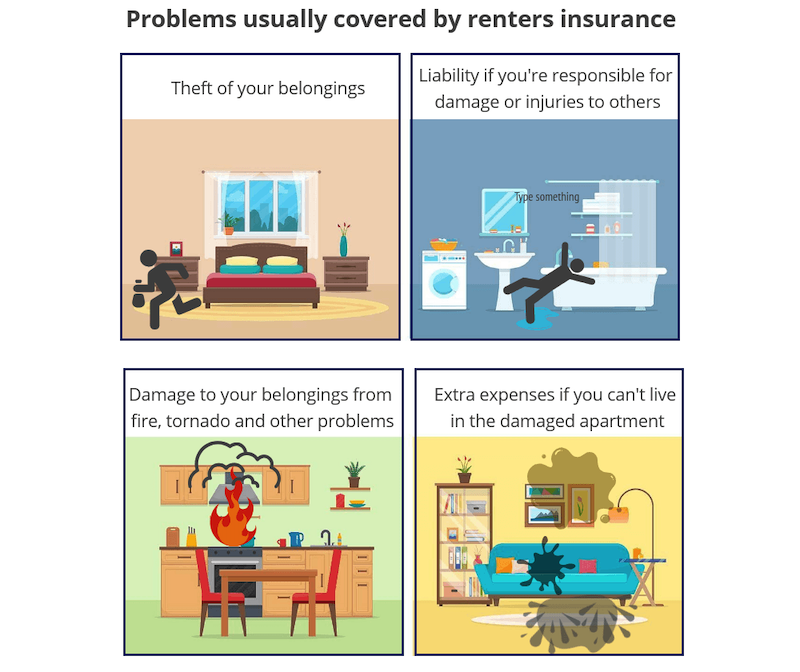

Landlord Insurance vs. Renter’s Insurance

These are two totally different things. You need one, and you should absolutely require your tenants to have the other.

Landlord Insurance (or Dwelling Policy) is what you buy. It’s specifically for non-owner-occupied properties and covers the big stuff: damage to the building from things like fire or wind, and liability protection. That liability part is critical. If a visitor slips on an icy sidewalk you forgot to salt, this insurance covers their medical bills and protects you from a lawsuit that could wipe you out.

Renter’s Insurance is what your tenant buys. It covers their personal belongings and their personal liability. I make it mandatory for every tenant, and I ask to be listed as an “additional interested party.” This just means I get a heads-up if the policy gets canceled.

Why is this a big deal? I had a tenant on a second floor leave a tub running, and it overflowed. The water ruined the laptop, TV, and furniture of the person living downstairs. Because the upstairs tenant had renter’s insurance, their policy paid for all the damage. It was a clean, simple fix. When I explain this to new tenants, I tell them it’s usually only $15-$25 a month. I frame it as a ‘good neighbor policy’ that protects them and their stuff for less than the cost of a few coffees a month.

Oh, and one more thing. If you own multiple properties, look into an umbrella policy. It adds an extra layer of liability protection on top of your other policies for a relatively low cost. It’s a smart way to shield your personal assets.

3. Tenant Screening: Your Most Important Job

Honestly, the quality of your tenants will make or break your experience as a landlord. Great tenants pay on time and respect the property. Bad tenants can cost you thousands in damage, legal fees, and lost rent. It’s tempting to rush to fill a vacancy, but putting the wrong person in your property is far more expensive than having it sit empty for an extra couple of weeks.

Your screening process should be a system—consistent, thorough, and fair for every single applicant.

I have a four-step process I never deviate from:

- The Pre-Screening Call: Before anyone sees the unit, I have a quick chat to cover the basics: move-in date, the rent and security deposit amounts, and our major policies (like no smoking or income requirements). This saves everyone a ton of time.

- The Application: At the showing, I provide a link to my online application. It must be filled out completely. It also includes a crucial signature line giving me permission to run their background and credit.

- Verification (The Real Work): This is where you separate yourself from the amateurs. You have to verify everything. Call their employer. Ask for pay stubs. And most importantly, call their current and previous landlords. The previous landlord has no reason to lie just to get rid of them. My go-to question is always: “Would you rent to them again?” The pause before they answer tells you everything.

- The Background & Credit Check: I use a professional, FCRA-compliant service for this. There are a bunch of great ones out there, like SmartMove, RentPrep, or even the tools built into Zillow Rental Manager. The cost is usually between $35 and $55, a fee I pass along to the applicant as part of the application. I’m not looking for a perfect credit score, but I am looking for a pattern of responsibility. An eviction history is a huge red flag and almost always a deal-breaker.

By the way, what do you do with a great applicant who has no rental history, like a recent grad? This is a common one. In these cases, I lean more heavily on their income verification and credit history. If I’m still on the fence, I might require a qualified co-signer. It’s all about finding ways to reduce your risk while still being fair.

4. Proactive Maintenance: Protect Your Investment

Your property is an asset that needs regular care. Too many landlords get stuck in a reactive cycle—they wait for a call about a broken pipe, then scramble to fix it. That’s stressful and way more expensive. The professional approach is proactive; it’s about spotting and fixing small issues before they become disasters.

Seasonal Checklists & The Pro-vs-DIY Question

A simple seasonal checklist is your best friend. In the spring, I’m cleaning gutters and getting the AC serviced before it gets hot. In the fall, it’s the furnace’s turn. Doing these routine checks helps you catch problems early.

A good rule of thumb is to know when to DIY and when to call a pro. Sure, you can probably handle changing furnace filters, replacing a toilet flapper, or touching up paint. But when it comes to certain jobs, trying to save a buck is just not worth the risk. For anything involving major plumbing, electrical work, or HVAC systems, you should ALWAYS call a licensed and insured professional. One faulty wiring job can lead to a fire, and that’s a liability you simply can’t afford.

Build Your Team and Budget for the Big Stuff

You can’t do it all. Start building a list of go-to pros: a reliable plumber, a good electrician, and a skilled handyman. How do you find them? The best referrals I’ve ever gotten came from other landlords. Join a local Real Estate Investors Association (REIA) or find a landlord group on Facebook for your area. Those folks will give you the unfiltered truth.

And please, please budget for repairs. They are a certainty. A good starting point is the 1% Rule: plan to set aside about 1% of your property’s value each year for maintenance. You also need to save for Capital Expenditures (CapEx)—the big-ticket items like a new roof or furnace.

Think of it this way: a new roof might cost $10,000 and last 20 years. That comes out to $500 a year, or about $42 a month, that you should be putting aside just for the roof. If you don’t, that $10,000 bill is going to be a very nasty surprise someday.

5. Tenant Relations: The Human Element

At the end of the day, this is a customer service business. Your tenants are your customers. A good relationship based on mutual respect is worth its weight in gold because happy tenants stay longer. That dramatically reduces your single biggest expense: turnover.

It all comes down to a few simple things.

Communicate well. Be firm, fair, and consistent with the rules for everyone. And remember that while you own the property, they are paying for a home. Always respect their privacy and give proper notice before entering. A little respect builds a lot of goodwill and makes it much more likely they’ll take great care of your property and renew their lease.

Quick Disclaimer: This is all based on my own experience and is meant to be helpful information, not official legal or financial advice. Laws change and vary by location, so you should always chat with a local attorney and a good accountant to make sure you’re doing everything by the book.